Support

Support GST Cancellation

Cancellation of GST registration is not a hard work as Indian government GST Portal has provided a simple an easy step by step procedure to finally cancel the GST registration of migrated taxpayers through newly implemented feature. Goods and services tax which was implemented recently and to be exact on 1st July 2017 with a lot of promises and work on progress tagline, is known to be subsuming all the indirect taxes into one. All the business units are exempted from paying GST which are under the turnover of 20 lakhs annually and all the business units above this exemption limit have to be registered under the GST.

The registration part has been discussed everywhere and has been understood manifold by guides and articles, but now there comes a chance to cancel the registration under GST by the taxpayer itself or by any governing authorities. The cancellation option is for migrated taxpayer only who wants to cancel their registration on GST.

By far we have got the confirmation that the business organization can cancel their registration by the means o the recently popped up feature on the GSTN portal, but the cancellation feature is limited to only 3 entities who can initiate the cancellation of registration:

- The taxpayer himself

- GST officer

- A legal heir of the taxpayer

The cancellation of the registration can be initiation in some cases like the death of the taxpayer. While the registration can also be done voluntarily but only after one or more years are elapsed starting from the date of GST registration.

GST Authorities Cancelled 1.63 lakh Registrations

Goods & services tax (GST) authorities have cancelled over 1.63 lakh registrations in October and November of taxpayers who have not filed their GSTR-3B returns for more than six months. The council started serving notices to taxpayers who did not file their GSTR-3B returns for the past six months or more and then cancelled their registration as per the procedure.

Conditions, When a Taxpayer Can Cancel the GST registration?

- Discontinuance or closure of the business

- Taxable person ceases to be liable to pay tax

- Transfer of business on account of amalgamation, merger de-merger, sale, leased or otherwise

- Change in constitution of business leading to change in PAN

- Registered voluntarily but did not commence any business within specified time

- A taxable person not liable any longer to be registered under GST act

Who All Cannot File the Cancellation of GST Registration?

- Taxpayers registered as Tax deductors / Tax collectors

- Taxpayers who have been allotted UIN

Steps for Cancellation of GST Registration Online on GST Portal

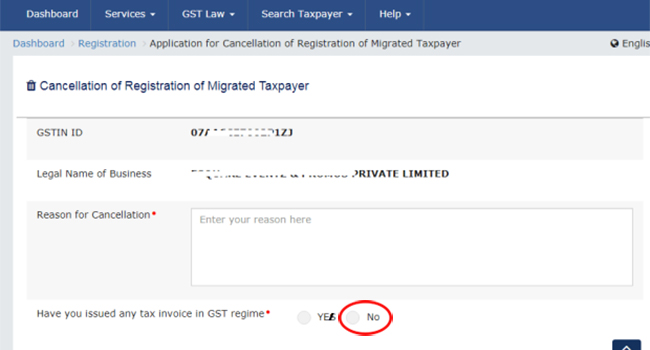

The GSTN portal is live with the cancellation of GST registration for the migrated taxpayers. All the taxpayers who have not issued any invoice after the registration can opt for this service. The individual can fill out form GST REG 16 in case he has filled any tax invoice.

Steps for cancellation of GST registration for the migrated taxpayer:

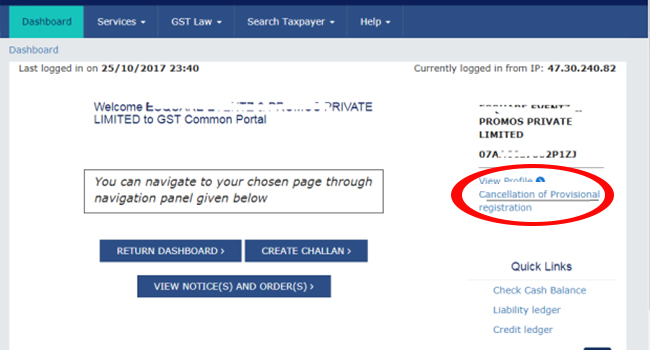

- Login with username and password on GST portal

- Then click on the tab ‘Cancellation of provisional registration’

- After which a popup will ask that if a taxpayer has raised any tax invoice in the period of GST

- Select ‘No’

- After the selection, the taxpayer will have to go through verification and have to submit all the form related details along with the digital signature/EVC

OUR BLOGS

- 1. Under which circumstances can a Tax Official initiate for cancellation of GST registration?

-

Suo Moto Cancellation of registration may be initiated by the Tax Official for various situations as mentioned in the provisions of GST law like: -

- Any Taxpayer other than composition taxpayer has not filed returns for a continuous period of six months

- Supplies any goods and / or services without issue of any invoice, in violation of the provisions of the Act or rules made thereunder, with the intention to evade tax

- Issues any invoice or bill without supply of goods and/or services in violation of the provisions of this Act, or the rules made thereunder leading to wrongful availment or utilization of input tax credit or refund of tax

- Collects any amount as representing the tax but fails to pay the same to the account of the Central/State Government beyond a period of three months from the date on which such payment becomes due

- Fails to pay any amount of tax, interest or penalty to the account of the Central/State Government beyond a period of three months from the date on which such payment becomes due

- Person is no longer liable to deduct tax at source as per the provisions of GST Law

- Person is no longer liable to collect tax at source as per the provisions of GST Law

- Person no longer required to be registered under provisions of GST Law

- GST Practitioner is found guilty of misconduct in connection with any proceeding under the GST Law.

- Discontinuation/Closure of Business

- Change in Constitution leading to change in PAN

- Ceased to be liable to pay tax

- Transfer of business on account of amalgamation, merger/demerger, sale, lease or otherwise disposed of etc.

- Death of Sole Proprietor

- Composition person has not furnished returns for three consecutive tax periods,

- Registration has been obtained by means of fraud, willful misstatement or suppression of facts. Etc.

- 2. Will I be intimated before the Suo Moto Cancellation of Registration?

-

Yes. Registration cannot be cancelled without a Show Cause Notice being given to taxpayer and a reasonable opportunity of being heard by the Tax Official. Thus, in case of Suo Moto cancellation of registration, a Show Cause Notice shall be issued by the Tax Official/ Proper officer to the taxpayer and taxpayer would be given a chance to file clarifications in the stipulated time limit.

- 3. What is the precondition for Suo Moto Cancellation of Registration?

-

There must be a valid reason for initiation of proceeding for Suo moto cancellation as specified under Section 29(2) of the CGST/SGST Act.

- 4. What is the duration within which I need to file a response for Show Cause Notice regarding Suo Moto Cancellation of Registration?

-

You need to provide response within the prescribed time limit of 7 working days’ time to file reply to the Show Cause Notice (SCN) using the Services > Registration > Application for Filing Clarifications link. If no response is given within prescribed 7 working days, the Tax Official can proceed with Cancellation of registration.

- 5. What shall be the effective date of cancellation of registration?

-

Effective date of cancellation will be the date as mentioned in the cancellation order.

- 6. Will the cancellation of registration means that I have no liabilities?

-

No, any liabilities prior to the date of suo moto cancellation will have to be paid by the taxpayer, irrespective of the fact that when determination of liabilities are done. Any liability which is related to that particular GSTIN is required to be paid by the taxpayer. It can be recovered later on even after the cancellation of GSTIN.

- 7. Will the cancellation of registration means that I have no liabilities?

-

Cancellation of registration under the CGST Act or SGST/UTGST or IGST Act shall be deemed to be a cancellation of registration under SGST Act / UTGST Act or CGST Act respectively and vice versa.

- 8. Will I be able to login after suo moto cancellation of registration?

-

Yes, you can login to the GST Portal after suo moto cancellation of registration.

- 9. Can I update my email and mobile after suo moto cancellation of registration?

-

You will not be able to amend registration after issuance of cancellation order. However, email address and mobile number can be updated till dues/ refund are cleared.

- 10. Can I submit returns of the earlier period after suo moto cancellation of registration?

-

You can submit returns of the earlier period (i.e. for the period before date of cancellation mentioned in the cancellation order), after suo moto cancellation of registration. However, you will not be allowed to file return or upload invoices for the period after date of cancellation mentioned in the cancellation order. Also, GSTP will not be able to carry out GSTP functions on your behalf for the period after the date of cancellation mentioned in the cancellation order.